You are here:Home >Newsletters>Archives

MHP NEWS

June 2021

We are approaching the end of the 2021 tax year. That means, it's also time to get your tax records together and start the new financial year off on the right foot!

If any or your individual or business circumstances are changing from 1 July, let us know so we can assist you to meet all your necessary obligations and ensure you start the year organised and prepared.

In this newsletter you will find;

- In House News

- What's changing for you on 1 July

- Summary of the Federal Budget that was released in May

- Financial Housekeeping for 2021 year end

- What we need from you when preparing your tax

In House News

Ag Grow Emerald

McDonnell Hume Partners is heading to Ag Grow Emerald this year!

Ag Grow Emerald runs from the 24th to the 26th of June at the Ag Grow Felid day site on the Capricorn Highway. You will find us at site 16 in the Emerald Pavilion. Pop by and say hi to Jean- Pierre who will be the face of MHP over the course of the event.

We'll have goodies to give away, knowledge to share, fact sheets to take and more.

Its more than just a field day!

Client Drop Box

Tired of tackling the stairs to drop your work/info at reception!?

We will be installing a 'client drop box' at the bottom of our stairs!

We will have a secure, wall mounted mailbox that you can drop your client info, signed tax returns, USB's etc in for us to collect. We will empty several times a day and take care of it for you.

Of course you are always welcome at reception should you wish to hand it over personally.

What's New and Changing from 1 July 2021?

Super Guarantee rate to increase to 10%

On July 1 2021, the Superannuation Guarantee (SG) rate will rise from 9.5% to 10%.

So if you are a business with employees, you will need to ensure your payroll and accounting systems are updated to incorporate the increase to the superannuation rate.

The below link will provide you more information on the increase and tools to determine if your employees are eligible for super (including contractors treated as employees for super purposes).

SG will increase at a rate of 0.5% over the next 5 years to reach 12% by 1 July 2025.

https://www.ato.gov.au/Business/Business-bulletins-newsroom/Employer-information/Super-Guarantee-rate-rising-1-July/

Please also note also from 1 July 2021, where an employee does not have a superannuation fund, you can no longer set up a default fund. You will first need to contact the ATO to see if the employee has any existing superannuation funds to connect to. Only when the ATO confirms that there are no existing super funds connected to the employee, can you you use your default fund.

Company Tax Rate Reductions

From 1 July 2021, the company tax rate for base rate entities will reduce to 25%.

|

|

2020-21 |

2021-22 |

| Base rate entities* |

26% |

25% |

| Other corporate tax entities |

30% |

30% |

*aggregated turnover less than $50m and no more than 80% of the company's assessable income is base rate entity passive income.

Single Touch Payroll (STP)

From July 2021 Single Touch Payroll (STP) will apply to most businesses. This will now include small businesses (those with fewer than 19 employees) and business with closely held employees ie directors of family companies, salary and wages for family employees of a business).No further extensions will be granted.

However, employers with closely held employees, some concessions on how you report is being offered. Employers in this category can report in actual real time, report actual payments quarterly or report a reasonable estimate quarterly.

If you fit in to this category and need assistance please contact us to assist you with the transition.

Superannuation Concessional & Non-Concessional Contribution Caps

From July 2021, the superannuation contribution caps will increase. This means you are able to contribute more to your superannuation fund (as long as you have not already reached your cap).

The concessional contribution cap will increase from $25,000 to $27,500.

A reminder that concessional contributions are contributions made to your superannuation fund before tax (like superannuation guarantee).

The non-concessional cap will increase from $100,000 to $110,000. Remember, non concessional contributions are after tax contributions made to your superannuation fund.

The 'bring forward' rule allows those under 65 years to contribute three years worth of non-concessional contributions to their superannuation fund in one year. So, from July, people in this category can contribute up to $330,000 in one year (Superannuation balance rules will apply).

Federal Budget Summary

As the 2020/2021 budget was only released in October last year due to the Covid-19 crisis, so the 2021/2022 budget release was slim.

The 2021/2022 budget is focused around continuing Australia's recovery from Covid-19 and its economic impacts.

The following are some of the budget items most relevant to you in the tax and accounting world.

Personal Income Tax Changes

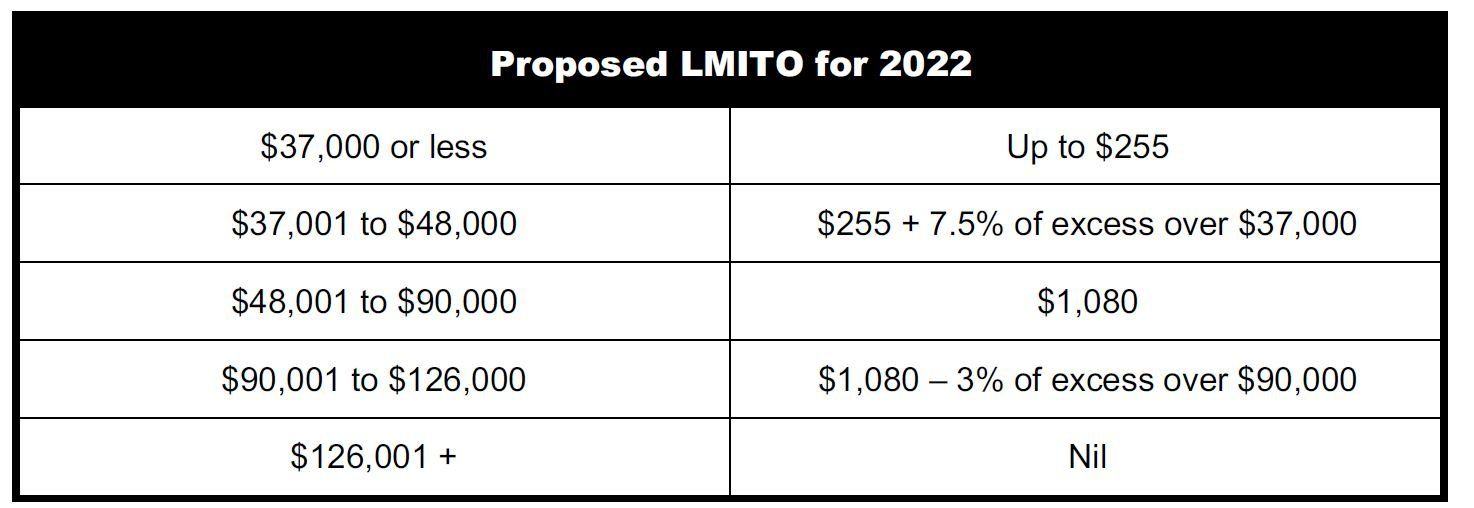

Low and Middle Income Tax Offset (LMITO)

The Government has proposed it will retain the LMITO for one more income year. Therefore, it will be available for the 2022 income year.

The LMITO is a non-refundable tax offset that provides relief for low and middle income taxpayers and is available in addition to the Low Income Tax Offset ('LITO').

Below are the proposed LMITO changes from the 2022 year.

Increasing the Medicare Levy Low Income Thresholds

Medicare low income thresholds for singles, families and seniors and pensioners will increase for the 21 income year as follows;

Singles threshold will increase from $22,801 to $23,226.

Family threshold will be increased from $38,874 to $39,167.

Single Seniors and pensioners threshold will increase from $36,056 to $36,705.

The family threshold for seniors and pensioners will be increased from $50,191 to $51,094.

For each dependent child or student, the family income thresholds increase by a further $3,597.

Individuals Claiming Self-Education Expense Deductions

The first $250 of a specified course or education expense (self education expense) is currently not tax deductible. The Government will remove this omission and it will apply from the income year after the date of legislation being passed.

Changes Affecting Business Tax Payers

Temporary Full Expensing Extension

Temporary full expensing that the Government announced amendments to in the last budget became law on 14 October 2020. The Government have now announced that temporary full expensing will be extended for a further 12 months.

This means that eligible businesses with aggregated annual turnover or total income of less that $5 billion can deduct the full cost of eligible depreciable assets of any value acquired from 7.30pm 6 October 2020 and first used or installed ready for use by 30 June 2023.

This can be fully deductible upfront rather than being claimed over the asset's life.

For businesses with an aggregated turnover under $50 million, the full expensing also applies to second-hand assets.

From 1 July 2023, normal depreciation rules will apply and the instant asset write-off threshold for eligible businesses will revert back to $1,000.

Temporary loss carry-back extension

The 2021/22 federal budget release also saw the extension of the loss carry back measure. Companies with aggregated turnover of less than $5 billion can carry back (utilise) tax losses from the 2021 income year to offset previously taxed profits as far back as the 2019 income year when a tax return is lodged for the 2021 income year.

Superannuation Related Changes

Removing the $450 per Month Threshold Superannuation Guarantee eligibility.

Currently employees need to earn $450 per month to be eligible to be paid superannuation guarantee from an employer. This threshold will be removed so all employees will be paid superannuation from their employer regardless of the income earned.

This will come into effect from the start of the income year the legislation is enabled.

Financial Housekeeping for Year End

Before you roll-over your software

Before rolling over your accounting software for the new financial year, make sure you:

- Do not perform a Payroll Year End function until you are sure that your STP finalisation declaration is correct and printed. Always perform a payroll back-up before you roll over the year.

Employee reporting

Single touch payroll

Where payments to employees have been reported to the ATO through single touch payroll, a finalisation declaration generally needs to be made by 14 July 2021 for employers with 20 or more employees and 31 July 2021 for those with 19 or fewer employees.

Payment summaries do not have to be provided to employees. Instead, employees will be able to access their Income Statement through myGov.

Reportable Fringe Benefits

Where you have provided fringe benefits to your employees in excess of $2,000, you need to report the FBT grossed-up amount. This is referred to as a `Reportable Fringe Benefit Amount' (RFBA).

Do you need to do a stocktake?

Businesses that buy and sell stock generally need to do a stocktake at the end of each financial year as the increase or decrease in the value of stock is included when calculating the taxable income of your business.

If your business has an aggregated turnover below $10 million you can use the simplified trading stock rules. Under these rules, you can choose not to conduct a stocktake for tax purposes if the difference in value between the opening value of your trading stock and a reasonable estimate of the closing value of trading stock at the end of the income year is less than $5,000. You will need to record how you determined the value of trading stock on hand.

Claiming Tax Deduction for Quarter End Super payments to Employees

If you use the Small Business Superannuation Clearing House (SBSCH) and are intending to to pay your employees quarter end superannuation prior to 30 June to claim a tax deduction then you need to be aware of the following.

Payments made must be accepted by the SBSCH on or before 23rd June 2021. This allows processing time for the payments to be received by the employees superannuation funds before the end of the 20/21 income year.

ATO Focus Areas

Cryptocurrency Under the Microscope

This tax time, the ATO are putting the spotlight on cryptocurrency. The ATO are concerned that many taxpayers think their cryptocurrency gains are tax-free or only taxable when the holdings are cashed back onto Australian dollars. If you fall into this category you need to keep good records of all your cryptocurrency transactions.

If you have traded in cryptocurrency, please ensure you let us know so we can treat it appropriately in your 2021 income tax return.

Work Related Expenses- Getting it Right

Another focus area for the ATO this tax time is work related expenses. You need to get it right! If you are claiming any work related expenses, you need to remember these three very important rules:

- You spent the money and were not reimbursed

- The money you spent was directly related to earning income

- You have a record to prove your expenditure

Knowledge Shop. (May 2021). Updates. Budget 2021-22: The Balancing Act, 1-32. NTAA. (May 2021). Alerts & Updates. 2021.22 Budget Handout, 1-6.

What we need from you to prepare your tax

When gathering up your tax records at the end of the financial year, the following list is a good checklist of what we will require from you to complete your income tax returns.

Individuals:

- Income statement

- Tax statements of managed investment funds

- Interest income from banks and building societies

- Dividend statements for dividends received

- For share sales or purchases, the purchase and sale contract notes

- For real estate sales or purchases, the solicitor's correspondence for the purchase and sale

- Rental property statements from real estate agent and details of other expenditure incurred

- Work related expenses

- Self-education expenses

- Travel expenses

- Donations to charities

- Health insurance and rebate entitlement

- Family Tax Benefits received

- Commonwealth assistance notices

- IAS statements or details of PAYG Instalments paid

- Details of any transactions involving cryptocurrency (e.g., Bitcoin)

- Details of any income derived from participating in the sharing economy (e.g., Uber driving, rent from AirBNB, jobs completed through Airtasker etc.,)

Business:

- Accounts data file (MYOB, Quickbooks, access to Xero)

- Debtors & creditors reconciliation

- Stocktake if applicable (or, if your business is a Small Business Entity, use the simplified trading stock rules mentioned)

- 30 June bank statements on all relevant loan documents

- Documents on new assets bought or sold, including the date you entered the contract and the date the asset was first used or installed ready for use

- Payroll reconciliation

- Superannuation reconciliation

- Bank statements on operating accounts

- Cash book (if applicable)

- 30 June statements on any investment or operating accounts

Please contact us for any clarification on any tax matters or issues pertaining to your individual circumstances.

Be sure to check out the links below and keep up to date with the due dates for your tax obligations.

See you in September 2021

Kind Regards

The Team

McDonnell Hume Partners